Real-world asset (RWA) tokenization is moving from the crypto niche to institutional infrastructure faster than most participants realize. Yet most retail participants still cannot answer three basic questions: what exactly do you hold when you acquire an RWA token? Who enforces your rights if something goes wrong? And can you actually transfer when you need to? This guide cuts through the noise. You will learn what RWA tokens are, how they work from creation to redemption, where the real growth is happening, and how to analyze opportunities before committing a single dollar.

Key Takeaways

- Fractional ownership access — RWA tokens make global real estate access possible with small amounts of capital.

- Legal and distribution-layer risks — Distribution-layer activity is limited, and rights depend on legal structures, not just blockchain technology.

- Analyze before joining — Use a clear participant checklist to evaluate distributions, security, and legal enforceability before acquiring any RWA token.

- Growth in RWA ecosystem — RWA tokenization ecosystem size is rapidly rising, but real estate remains a small share compared to Treasuries.

What are real-world asset (RWA) tokens?

RWA tokens are blockchain-based digital representations of ownership rights or economic exposure to off-chain assets. Think of them as digital certificates that attest to your stake in something physical or financial, whether that is a rental apartment in Dubai, a U.S. Treasury bond, or a private credit fund. As explained by tokenization researchers, these tokens enable fractional ownership and blockchain programmability while remaining anchored in traditional legal structures.

The range of assets being tokenized is broader than most people realize:

Real estate: residential, commercial, and industrial properties.

Government securities: U.S. Treasuries and sovereign bonds.

Private credit: business loans and structured debt.

Commodities: gold, oil, and agricultural products.

Funds: private equity and hedge fund shares.

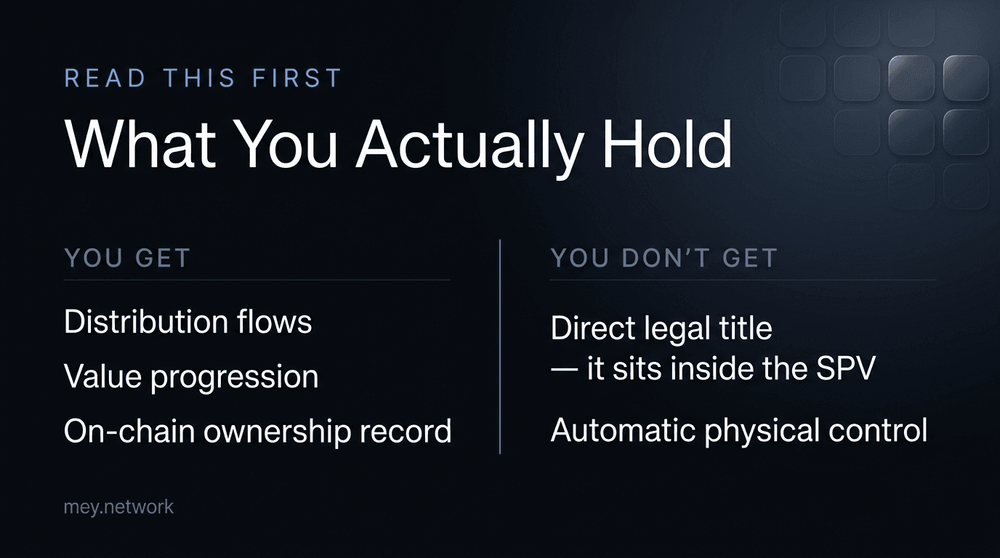

One critical distinction every participant must understand: holding an RWA token does not automatically mean you own the underlying asset. In most cases, you hold economic exposure, meaning you receive distribution flows and value progression, but the legal title sits inside a corporate structure. Mey Network is one platform building infrastructure to make this global access cleaner and more transparent for retail participants.

For a broader primer on how stablecoins and RWA tokens overlap, the stablecoin RWA explainer is worth reading before you go deeper.

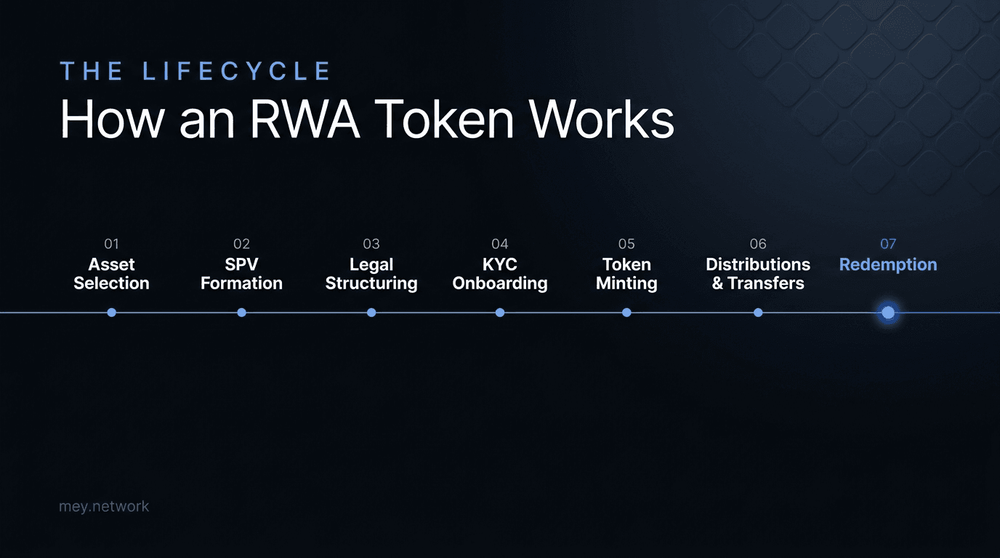

How RWA tokens work: the lifecycle explained

Understanding the mechanics behind RWA tokens is what separates informed participants from those who get burned. The full lifecycle covers asset structuring, legal definitions, KYC onboarding, token minting, transfers, value accrual, and eventual redemption. Each stage carries its own risks and participant checkpoints.

Here is how the process typically unfolds for a tokenized real estate deal:

Asset selection: a property is identified and appraised by an independent valuer.

SPV formation: a Special Purpose Vehicle (SPV) is created to legally hold the asset, ring-fencing it from the issuer's other liabilities.

Legal structuring: participant rights, distribution rules, and exit terms are defined in offering documents.

KYC and onboarding: participants complete identity verification before they can acquire tokens.

Unit minting: tokens representing fractional shares of the SPV are created on-chain.

Distribution-layer activity and distributions: token holders receive rental flows or interest distributions, and may transfer tokens on distribution venues.

Redemption: at maturity or upon exit, tokens are burned, and proceeds are distributed.

Setup typically takes 4 to 8 weeks. Redemption can take longer depending on asset distribution-layer depth and legal jurisdiction. Fractional real estate participation through platforms with clear SPV structures gives you the most protection at each stage.

Pro tip: only allocate to RWA projects with independently audited legal structures. An audit of the smart contract alone is not enough. The legal wrapper around the asset matters just as much as the code.

Where RWA tokens are gaining traction: real-world growth and key statistics

Now that you know the mechanics, look at where RWA tokens are actually thriving. The numbers tell a story that surprises most people.

tokenized Treasuries, by contrast, have crossed $10B. That gap is not a sign that real estate tokenization is failing. It reflects the complexity of legal structuring and the slower pace of regulatory clarity in property ecosystems globally.

Real estate tokenization is not behind. It is just harder. The legal lift is significantly greater than wrapping a Treasury bond in a token.

For retail participants, the takeaway is clear. The infrastructure is maturing fast, but real estate tokenization is still in its early innings. That means higher potential upside and higher risk compared to tokenized Treasuries.

- U.S. Treasuries

- tokenization maturity: High

- Typical distribution range: 4 to 5%

- Real estate

- tokenization maturity: Medium

- Typical distribution range: 6 to 16%

- Private credit

- tokenization maturity: Medium

- Typical distribution range: 8 to 15%

- Commodities

- tokenization maturity: Low

- Typical distribution range: Price-linked

The nuances and complexities behind RWA tokens

Behind the numbers, it is essential to understand the legal, technical, and operational nuances that affect your token ownership. These are the details that most marketing materials skip.

Hybrid custody is one of the most misunderstood aspects. Not everything is on-chain. The token lives on the blockchain, but the underlying asset, the property deed or bond certificate, is held off-chain by a custodian. If that custodian fails, your token may become worthless regardless of what the smart contract says.

Oracles are another critical dependency. Oracles are data feeds that bring real-world information (like property valuations or rental flows) onto the blockchain. If an oracle is manipulated or goes offline, the token's on-chain data becomes unreliable. This is a real and underappreciated risk.

Other nuances that affect your position include:

Permissioned transfers: most RWA tokens use ERC-3643 compliance standards or similar frameworks that restrict who can hold or transfer the token. You cannot simply send it to any wallet.

Redemption delays: cashing out is rarely instant. Fees, lock-up periods, and asset-transfer timelines can delay your exit by weeks or months.

SPV insolvency protection: a well-structured SPV legally separates the asset from the issuer, protecting participants if the platform goes bankrupt. As detailed in the RWA tokenization analysis, this ring-fencing is one of the most important participant protections available.

- Participant protection

- Trust structure: Moderate

- SPV structure: Strong

- Legal ring-fencing

- Trust structure: Partial

- SPV structure: Full

- Regulatory clarity

- Trust structure: Varies

- SPV structure: Generally clearer

- Common in

- Trust structure: Smaller deals

- SPV structure: Institutional deals

Pro tip: always read the offering's legal disclosures and redemption terms before acquiring. If the document does not clearly explain how and when you can exit, treat that as a red flag.

Risks and misconceptions: what most participants get wrong

Having covered complexities, now spotlight the risks and realities you must grasp before joining. The biggest misconception in RWA tokenization is that blockchain equals deep distribution layer. It does not.

Minting RWA units is relatively straightforward. Exiting positions, however, remains significantly more difficult due to limited secondary-market activity.

There are four primary danger zones: counterparty and custody failure, low distribution-venue activity despite tokenization, regulatory classification concerns, and oracle manipulation. Each of these can erode or eliminate your position.

Here is what most retail participants get wrong:

Distribution-layer overestimation: real estate RWA tokens may only circulate once per year on distribution venues. Compare that to stocks or crypto, which move every second.

Legal enforceability gap: the technology is only as strong as the legal structure behind it. A token without enforceable rights is just a digital receipt.

Regulatory reclassification risk: In some jurisdictions, regulators may classify your token as a security, triggering compliance requirements that freeze transfers or force redemptions.

Counterparty concentration: even on-chain systems rely on off-chain actors, custodians, property managers, and legal trustees. Their failure is your problem.

Distribution confusion: high advertised distribution rates often reflect gross flows before fees, taxes, and vacancy costs. Net rates can be significantly lower.

For a deeper look at common misconceptions, the gap between marketing claims and operational reality is often substantial.

How to analyze an RWA token as a retail participant

Concluding the educational content, here is a practical framework for evaluating any RWA token opportunity before you allocate.

Start with these six due diligence steps:

Legal structure review: Is there an SPV? Is it independently audited? Who holds the legal title?

Custody clarity: Who holds the underlying asset? What happens if the custodian fails?

Cash-flow access: How and when do you receive rental flows or interest? Is it automated on-chain or manual?

NAV tracking: Does the platform publish regular net asset value updates with third-party verification?

Jurisdictional risk: Where is the asset located, and where is the issuer registered? Both matter for legal enforceability.

Redemption terms: Can you exit? When? At what cost?

Prioritizing legal structures, transparent custody, strong on-chain metrics, and real distribution rates from underlying cash flows is the foundation of sound RWA participation. High-volatility token price progression is a bonus, not a strategy.

Pro tip: Avoid any RWA offering that lacks an independent legal audit or does not clearly document its redemption process. Platforms that cannot answer these questions simply are not ready for your capital.

For context on where the sector is heading, the RWA sector forecasts project significant growth through the end of the decade, making early due diligence habits even more valuable. Evaluating RWA token deals with a structured checklist puts you ahead of most retail participants in this ecosystem.

Next steps: exploring fractional real estate with trusted partners

You now have the foundational knowledge to approach RWA tokens with clarity and confidence. The next step is finding platforms that meet the standards you have just learned to demand.

Mey Network is built specifically for retail and individual participants who want access to vetted, tokenized real estate opportunities globally. The platform combines transparent legal structuring, on-chain distribution, and a purpose-built blockchain for RWAs, giving you the infrastructure that the due diligence checklist above actually requires. Before committing capital anywhere, revisit the participant checklist from this guide. Ask every platform the same six questions. The ones that answer clearly and completely are the ones worth your attention. Mey Network is designed to answer all of them.

Frequently asked questions

Do RWA tokens guarantee direct legal ownership of an asset?

Most RWA tokens offer economic exposure or rights via a legal structure, not direct title to the property or physical asset itself. Your rights depend entirely on the legal documents behind the token.

How fluid are real estate RWA tokens for retail participants?

Despite being tokenized, real estate tokens circulate infrequently, sometimes only once per year, making them far less fluid than cryptocurrencies or stocks. Always check distribution-venue activity before acquiring.

What key risks should I look out for when acquiring RWA tokens?

The main risks include custody failure, regulatory issues, oracle manipulation, and low distribution-layer activity. Always verify that the platform has transparent audits and clearly documented legal structures.

Are distribution rates from RWA tokens reliable?

Real estate RWA tokens can distribute 6 to 16% annually, but those rates depend on underlying property performance and legal enforceability. There is no guaranteed flow, and net rates after fees are often lower than advertised.